In my last blog, I looked at the types of jobs being created in Auckland, over the period 2001 to 2016. Of note has been the big increase in the number of jobs in the professional, science and technical services sector (sector M in the ANZSIC). In this blog I want to look more closely at this sector.

Maybe one of the roles of planning is to positively support the growth of areas of employment where the city has a comparative advantage.

The relative importance of the sector for Auckland, compared to the national economy, can be assessed in simple terms by calculating a location quotient. Infometrics, in their Auckland Economic Profile web page (1) note that:

Maybe one of the roles of planning is to positively support the growth of areas of employment where the city has a comparative advantage.

The relative importance of the sector for Auckland, compared to the national economy, can be assessed in simple terms by calculating a location quotient. Infometrics, in their Auckland Economic Profile web page (1) note that:

A high concentration of certain industries in an area can be indicative of the area having a comparative advantage in these industries. This comparative advantage may be a result of the area’s natural endowments, location, skill profile, or other reasons.

Location quotients (are used) to identify what industries an area may have a comparative advantage in. An area has a location quotient larger than one when the share of that industry in the area’s economy is greater than the share of the same industry in the national economy.

Industry sectors in Auckland that have a location quotient greater than 1.1 are as follows, based on 2016 data.

Figure 1: Location Quotients over 1.1, Auckland Region, 2016

As a comparison, the location quotient for sector “C” - manufacturing - is 0.97.

The location quotients suggest that Auckland’s economy, beyond those parts of the economy that serves the resident population and/or is basically the same as the rest of the country, really falls into three groups:

- Warehousing and distribution

- Financial, insurance and banking

- Professional services.

A more fine grained analysis of industry sectors will reveal further clusters. For example, there will be some types of manufacturing activities that are concentrated in the city.

The M sector is relatively important. It has a location quotient of 1.34, which is quite high.

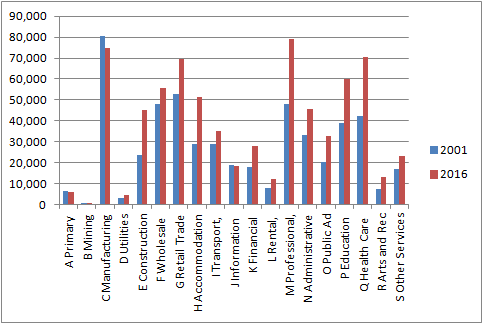

This is, however, a static picture. Comparing location quotients in 2001 and 2016 shows some changes in relative concentration. The table below lists the location quotients for 2001 and 2016, as well as the change in the number of people employed in the sector between these dates, for the Auckland Region.

Table 1: Location Quotients 2001 and 2016, and employment change.

Sector

|

LQ 2001

|

LQ 2016

|

Change in employment 2001 to 2016

|

F Wholesale Trade

|

1.62

|

1.49

|

7,600

|

I Transport and Warehousing

|

1.14

|

1.15

|

6,300

|

J Information Media and Telecoms

|

1.31

|

1.48

|

-300

|

K Financial and Insurance

|

1.37

|

1.43

|

9,800

|

L Real Estate Services

|

1.14

|

1.17

|

4,400

|

M Professional, Scientific and Technical

|

1.31

|

1.34

|

31,000

|

So over the period 2001 to 2016, Auckland’s relative strength in the wholesale trade sector dropped a bit, but employment increased. On the other hand, the region’s strong advantage in information, media and telecommunications increased, but employment actually dropped in this category.

The professional, scientific and technical sector increased in relative importance and increased substantially in employment, as did the financial and insurance sectors.

Sounds impressive, but in terms of incomes and wealth generated by the “M” sector, the sector tends to be at the lower end of the higher paying jobs. Looking at contribution to GDP, the following data is provided by Infometrics. It is the average GDP generated per worker in the Auckland Region, for 2016, by industry sector.

Figure 2: GDP per employee, by sector, Auckland Region 2016

The productivity of those in the rental, hiring and real estate sector (at over $300,000 per worker) is a bit hard to understand. As noted the FIRE sector (finance, insurance, information, real estate) tend to be sectors with the higher salaries and the biggest contribution to GDP per worker, but haven’t grown so much over the past few years.

The general picture is of Auckland’s labour market growing and changing over time. The growth of the professional, scientific and technical services sector has probably helped to diversify the economy somewhat, which is positive. But it has mostly been a picture of the expansion of the ‘base’ of the economy, with the relative decline in the banking, finance and insurance sectors. The M sector has risen in importance but this sector is not a big contributor to regional GDP on a per head basis.

Next up, where are the jobs in the ‘M’ sector located?

Starting at the Local Board level, the concentration of jobs in the sector in the inner Isthmus area (Waitemata Local Board) is very strong. See the following graph.

Figure 3: Employment location, sector M, 2016, by Local Board.

Taking a closer look at the Census Area Unit level, the following maps the number of people employed in the sector, again for 2016, by workplace location. There is a very strong clustering in the inner city area, with smaller outliers in Takapuna and Ellerslie. The Upper Harbour Local Board area has more people employed in the M sector, than Devonport-Takapuna, but in the Upper Harbour area, they are spread over a wider area.

Figure 4: Location of sector M employment, by census area unit, 2016

In terms of the other-side-of-the-coin, where do the people who work in the M sector live?

The following is a map of the percentage of people in full time or part time jobs employed in the M sector, for 2013 (the last census), by total number of people in work, by census area unit, by home location.

Figure 5: Location of home residence, people employed in sector M, 2013. Percentage of total workforce in Area Unit.

As about 11% of regional employment is in the M sector, then more than 10% of people who live in a census area unit and who are employed in the sector shows a relative concentration in terms of home location.

The map shows a very strong concentration of people living in the inner Isthmus and on the North Shore, as well as the rural North-West. The rural area units will not contain many people, so in actual numbers not percentages, most of the professional, technical and scientific sector workers will live in the city.

The fit between where people live and work in the M sector is pretty good from a planning perspective. Proximity helps a lot with accessibility. The sector will likely grow. More employment located in the city centre is positive, but will the future workers find a home location that fits their desires? If most of the future housing capacity is not in the Inner Isthmus or the North Shore coastal strip, then where do they go? Are they all foot lose workers who might decamp to other cities and countries if they cant find their perfect home in the city?

So where does this all lead us? Well one purpose of planning is to ensure that the city has an efficient labour market. Alain Bertaud in his paper ‘Cities as a Labour Market’ makes the case for planning to support market processes:

“Increasing mobility and affordability are the two main objectives of urban planning. These two objectives are directly related to the overall goal of maximizing the size of a city’s labor market, and therefore, its economic prosperity.

“Mobility” is the ability to reach any area of a metropolitan area in as short a travel time as possible, and “affordability” is the ability of households and firms to locate in whichever area they deem will maximize their welfare”.

Sounds good. But is it that simple? Whose mobility and affordability do you plan for? Do we support the growth of the M sector, or try to slow the relative decline of the higher paying FIRE sector and its bigger contribution to GDP? Will improving affordability of the inner Isthmus and coastal areas (basically, a lot more houses in these areas) mean that the appeal of these suburbs to workers in the M sector will actually decline as lifestyle is important to them (being mostly city hipsters?). Or do you put your money into improving accessibility from other locations, such as from out in the rural north-west?

Next blog - what about all the other workers, especially the lower paid and less skilled? Where do they live and work? (1) https://ecoprofile.infometrics.co.nz/Auckland/Gdp/ComparativeAdvantage