The RMA is again being blamed for soaring house prices. There is a ‘shortage’ of houses, with this shortage caused by restrictive zonings and district plans that are slow and cumbersome to change. But is it all a bit of a supply myth?

But as I have pointed out a number of times (as have others), a lot depends on how you calculate the shortage, and what you assume to be a reasonable response between demand (population growth) and supply (a dwelling being built).

Previously I have looked at issues like:

- Possible over estimaiton of migration flows and population growth

- The composition of demand, and the extent to which recent population growth has been driven by migration and uncertainty around the intentions of younger people on worker visas

- The lag between population growth occurring and houses being built. Evidence is that there is at least a two to three year gap between a building permit being issued and a completion certificate being signed off.

Time to have another go.

Statistics NZ have updated their yearly estimates of population growth in the light of the 2018 census. So I thought it would be good to re-run the numbers on demand and supply. I have done this for the two ‘hot’ property markets of Auckland and Queenstown.

Stats NZ provide an annual estimate of resident population for all Council areas. The most recent set for 2020 says that the estimated resident population (ERP) of each area is based on the 2018 Census usually resident population count, with updates for:

- residents missed or counted more than once by the census (net census undercount)

- residents temporarily overseas on census night

- reconciliation with demographic estimates for ages 0-14 years

- births, deaths, and net migration between census night and the date of the estimate.

The estimated resident population is not directly comparable with the census usually resident population count because of these adjustments.

Stats NZ have completed an intercensal revision for estimates between June 2013 and June 2018, to reconcile with the estimated resident population 2018-base. This has seen some downward revision of previous estimates.

Based on these recent estimates I have attempted to estimate housing demand and supply over the period 1997 to 2020. A long time period is needed, as plannnig is a long term process.

As previously noted, a range of assumptions need to be made.

First up, demand for housing is based on annual population growth divided by the average number of people per occupied dwelling. The average number of people per occupied dwelling can be calculated at the time of each census, as follows:

Table 1: Auckland and Queenstown dwellings and resident population

This data gives me the following average number of people per occupied dwelling.

Table 2: Auckland and QLDC people per occupiued dwelling

Some people at this point suggest that the rise in the average number of people per dwelling is not an independent variable. It is a sign of rising unaffordability as people share living spaces due to high housing costs, when the trend should be for fewer people per dwelling (more choice and more space). Others have pointed out that in Auckland at least, other changes like a younger population and possibly more multi-generational households formed by migrants helps explain the increase.

For example, for Auckland, there has been a dramatic change in the composition of growth, and with it likely demand for housing between the 2000s and 2010s. The graph below shows the change in the number of residents by age band, from 1996 to 2018. Through the mid 1990s to mid 2010s, the dominant group were the high income earning 40 to 64 year olds, many of whom would be looking for a ‘new home’. From mid 2010s, the largest group by far are the younger 15 to 39 year olds, many of who may be living at home or in flatting type situations, or after a second (or more) hand home.

Figure 1: Demogrpahic change - Auckland Region

This change in demographics must change housing markets, reducing demand for new homes to buy, slowing the flow of homes into the stock of housing, while at the same timing raising the demand for existing houses.

To determine demand, I have used the above data from the census on people per dwelling. Spreading out these rates on an annual basis leads to an estimate of demand for dwellings.

Supply is based on building permits issued. Building permits issued does not necessarily accord with the number of dwellings that are consented by way of RMA processes. There is no reliable way of counting how many ‘RMA consents” for new dwellings are issued each year. It could be that dwellings enabled by the planning system in each year is way ahead of building consents issued.

For this exercise, I need to run off building consents. Supply of new houses is based on the number of building consents issued in the two years after the estimated demand. That is, I have assumed that there is a lag between population growth occurring and house plans being drawn up, building permits obtained and houses built. In other words, the number of houses built in any year will likely reflect what demand was at least two years prior. So matching annual population growth with building permits issued in that same year is miss-leading.

However, some building permits for new dwellings will involve the removal or demolition of an existing dwelling. Comparing the increase in the number of dwellings (occupied and unoccupied) counted by the census with the number of permits issued in the preceding period (but lagged by you years to account for time to complete a building) gives me a guide as to how many permits are for replacement dwellings. My estimate is that in Auckland, 94% of permits are for new dwellings (not replacements).

Table 3: New dwellings versus building consents for dwelling units

The data suggests some unders and overs. For example between 2006 and 2013, 33,465 dwellings were added to the housing stock in Auckland, yet in the period 2004 to 2011, over 50,000 building consents were issued. A large number of consents must not have been actioned, or they took much longer to complete than 2 years.

In my analysis I have used the average for the period 2001 to 2018.

In Queenstown, the net addition rate is closer to 97%.

Table 4: New dwellings and building consents for dwelling units - QLDC

Next allowance needs to be made for ‘unoccupied’ dwellings - second houses, holiday homes and the like. In Auckland, census data suggests that of the total housing stock added between 2006 and 2018, 10% were unoccupied dwellings. In QLD it is more like 25%. Unoccupied means clearly not occupied on the night of the census.

Table 5: Occpied dwellings - Auckland and Queenstown

To put it together, for example in 2016 to 2017, the population of Auckland City grew by 35,300. At a ratio of 3.29 people per household, this equals a demand for 10,740 new dwellings. In 2019, building permits for 13,754 dwelling units were issued. Assuming that 6% involved replacement of an existing dwelling, then 12,929 new dwellings were added to the stock (net growth). Of these 91% were for occupied dwellings, or 11,745 dwellings. This then equals a surplus of 1,005 dwellings. .

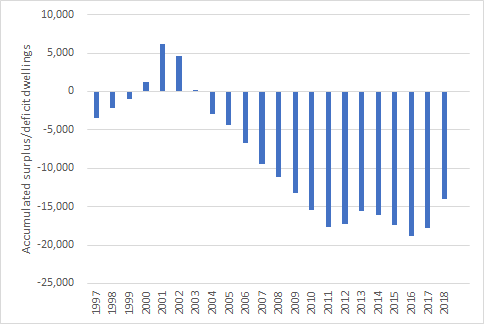

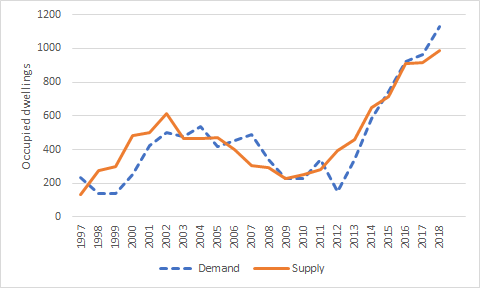

Below is the graph of the annual demand and supply from 1997 to 2018, for the Auckland Region. There is a ‘deficit’ over this period of 14,000 dwellings. The last 10 years (1999 to 2018) has seen a deficit of 3000.This is a lot less than the 30, 000 to 40,000 sometimes bandied about.

Figure 2: Auckland region: estimated housing demand and supply

The recent upward swing in building permits for new occupied dwellings suggests that the housing market is responding (as has the RMA). The deficit really built up in the post GFC period, and then it did take a while for the new build market to respond to the fast population growth between 2013 and 2018.

The accumulated surplus/deficit looks quite large, when graphed. See below. Since 2017, substantial inroads have been made.

Figure 3: Auckland Region housing surplus/deficit

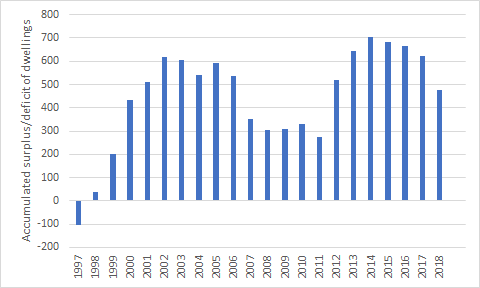

The same exercise can be undertaken for Queenstown Lakes District. Here there is a closer match between demand and supply, with some divergence over the period. Is this divergence enough to explain the large increases in house prices seen over this period?

Figure 4: Queenstown Lakes District demand and supply estimate

There is an accumulated surplus of 480 dwellings, using the methodology set out above.

Figure 5: QLDC housing surplus

Is there a supply myth? And if it is all a bit of a myth, what is the implications for the reform of the RMA and implementation of instruments like the National Policy Statement on Urban Development?

Planning needs to keep adding new capacity for more dwellings and businesses, but adding more capacity will not necessarily bring forward more affordable houses for households on low to moderate incomes. Urban quality is also important, and shouldn't be left behind in the dash for more capacity.